The DuitNow Plumbing Behind Fast Slot Withdrawals: What Happens in Those 2.3 Minutes

The 2.3-minute average Pirate777 publishes for slot withdrawals depends almost entirely on the rail underneath. This article is the technical companion to the architecture pillar — a closer look at the DuitNow infrastructure that actually moves the money, why it settles faster than legacy bank-transfer rails, what 24/7 means in practice, and how the eWallet sidecar rails fit in. The goal is to make the rail visible without disclosing operational specifics that don’t belong in public content.

DuitNow isn’t a bank — it’s PayNet’s real-time rail

Most people experience DuitNow through their bank’s app. That’s the user interface, not the system. The actual infrastructure is operated by Payments Network Malaysia (PayNet) under Bank Negara Malaysia’s regulatory framework. Banks are participants on the rail; PayNet runs the rail.

This matters for understanding withdrawal timing. When Pirate777 hands a withdrawal off to DuitNow Transfer, the transaction enters a shared real-time infrastructure that all participating Malaysian banks are connected to. The platform doesn’t need to maintain a bilateral connection with each bank — it connects to the rail, and the rail connects to every participating bank. That’s why a single platform architecture can serve withdrawals to accounts at every participating Malaysian bank — conventional or Islamic — with the same timing characteristics.

DuitNow Transfer vs IBG vs FPX — three different speeds

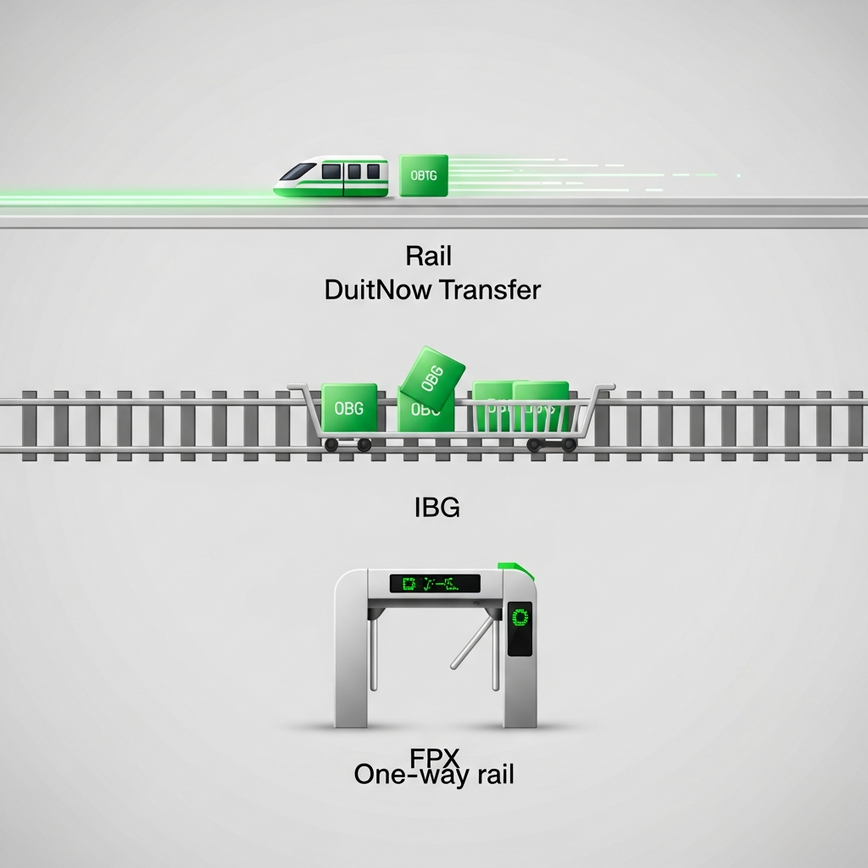

Malaysia has three relevant payment rails for moving money between banks. Confusing them is the single most common reason readers misread withdrawal speed claims.

- DuitNow Transfer. Real-time gross settlement. Each transaction settles individually as it’s submitted. Available 24/7 — both the rail and participating banks maintain DuitNow service continuously. This is the rail behind Pirate777’s 2.3-minute average for bank-account destinations.

- IBG (Inter-Bank GIRO). Batch settlement. Transactions are queued and settled at fixed cycles through the business day, typically next-cycle or next-business-day for the receiving end. Older platforms still use IBG for cost reasons. The 2.3-minute average does not apply to IBG.

- FPX (Financial Process Exchange). Real-time but transactional. Used primarily for inbound payment authorizations (deposits, online purchase clearings). Not used for outbound peer-to-account transfers in the way DuitNow Transfer is.

If you’ve seen a Malaysian platform advertise “fast withdrawals” without naming the rail, the implicit rail is often IBG — which is why “fast” can still mean hours or next-day. Naming the rail is half of being honest about timing.

Why DuitNow Transfer settles in seconds

The technical difference between batch settlement (IBG) and real-time settlement (DuitNow) is architectural, not effort-based. IBG aggregates transactions and runs settlement at fixed times; this saves processing cost and historically suited end-of-day banking operations. DuitNow Transfer settles each transaction the moment it arrives at the rail, debiting the sending bank’s settlement account and crediting the receiving bank’s account in the same atomic step. The handoff to the receiving bank’s internal systems then takes a fraction of a second to reflect on the destination customer’s app.

From Pirate777’s perspective, this means the platform’s payment layer issues a DuitNow Transfer instruction with the destination account details, the rail confirms settlement back to the platform almost immediately, and the receiving bank does its internal posting on its own systems. None of this involves a queue or a batch boundary — there’s no “next cycle” for a real-time transaction.

Why 24/7 actually works

The phrase “24/7” gets used loosely in payment marketing. For DuitNow Transfer it’s precise: PayNet maintains DuitNow service continuously, and participating banks maintain inbound and outbound DuitNow availability outside their core banking hours.

The qualification worth knowing: some receiving banks process inbound DuitNow on the same continuous schedule, while others reflect inbound DuitNow in the destination customer’s app on a slight delay during off-peak hours. The credit is on the bank’s books in real time; the user-visible balance update is a separate event handled by the bank’s app infrastructure. This is why a withdrawal can complete on Pirate777’s side while a destination bank app shows the inbound credit a few seconds later.

None of this involves the rail or the platform — both are running continuously. The “delay” some users experience on weekend nights is almost always the receiving bank’s user-side reflection, not the underlying rail.

The eWallet rails: TNG, GrabPay, Boost, ShopeePay

Slot withdrawals destined for an eWallet don’t strictly travel via DuitNow Transfer. Each eWallet operator runs its own near-real-time crediting infrastructure on the inbound side, with API integration to the platform’s payment layer.

- Touch’n Go eWallet. Near-real-time inbound crediting. The TNG balance reflects almost immediately on receipt.

- GrabPay. Near-real-time inbound crediting via Grab’s payment infrastructure.

- Boost. Similar pattern — near-real-time inbound crediting on Boost’s infrastructure.

- ShopeePay. Same pattern through Shopee’s payment layer.

From a player’s perspective, the timing characteristics are equivalent to DuitNow Transfer: single-digit minutes from withdrawal submission to balance visibility. The 2.3-minute average covers withdrawals to both DuitNow bank destinations and these eWallet rails together as one population.

What an eWallet withdrawal does not do: travel through DuitNow Transfer to a bank, then move from bank to eWallet. The eWallet integration is direct. This shortens the handoff chain by one institution.

Account-to-account vs DuitNow QR

DuitNow has two main user-facing modalities. The distinction matters for understanding what slot withdrawals use:

- DuitNow Transfer (account-to-account). Funds move from one account to another using the destination account number or DuitNow ID. This is what Pirate777 uses for slot withdrawals to bank destinations.

- DuitNow QR. Funds move via a scanned QR code, typically in retail or peer-to-peer contexts. This is for in-person and small-merchant payments, not platform-to-customer payouts.

If you’ve set up a destination account on Pirate777, you’ve provided account-to-account details (bank, account number). The platform doesn’t issue QR codes for withdrawals — there’s no scanning workflow on the user side at withdrawal time. The DuitNow QR rail is irrelevant to your withdrawal experience here.

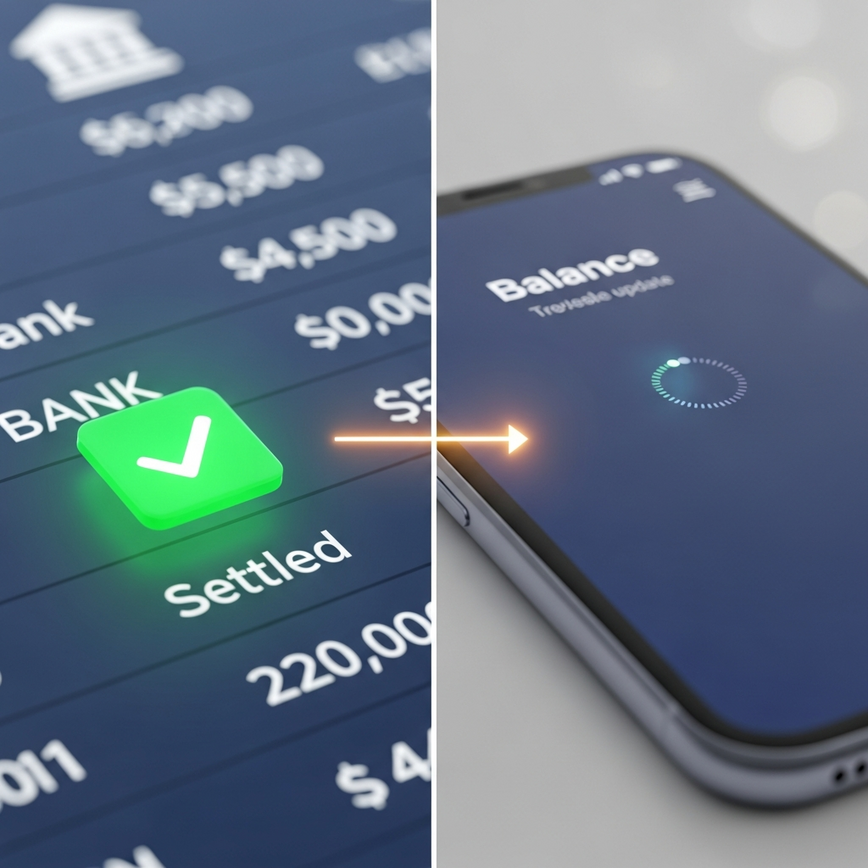

What “settled” means at each stage

The word “settled” gets used at several different boundaries in a withdrawal, and the differences cause confusion. From the rail’s perspective:

- Operator-side dispatch. The platform’s payment layer has issued the instruction to the rail. From Pirate777’s logs, the withdrawal is now “sent”. Not settled.

- Rail acknowledged. DuitNow has received the instruction, validated it, and committed to settlement. The platform sees a “confirmation” from the rail. This is settlement on the rail’s books.

- Receiver bank credit. The receiving bank has posted the credit to the destination customer account on its own internal ledger. The bank’s books show the customer is now richer.

- User-visible balance update. The receiving bank’s app or web interface reflects the new balance to the customer. This is the moment most users perceive as “the money arrived”.

The 2.3-minute average is end-to-end across all four boundaries. When a Pirate777 user sees “completed” status on the platform but the destination app hasn’t updated yet, they’re caught between boundary 3 (real) and boundary 4 (cosmetic). The money has arrived; the bank’s app is catching up.

The receiver-bank variable

Not all receiving banks reflect inbound DuitNow on their customer-facing apps at exactly the same speed. The differences are usually small — seconds, occasionally a minute — and don’t affect the rail’s settlement timing. They affect the user’s perception of when the money arrived.

Practical impact for Pirate777 users:

- If your destination bank typically reflects inbound transfers immediately on its app, your individual withdrawal experience tends to be at or below the 2.3-minute average.

- If your destination bank reflects inbound on a brief delay (some banks batch user-facing balance updates), your withdrawal still settles in real time on the bank’s books, but you may perceive a wait until the app catches up.

- Pirate777 doesn’t influence this; the bank’s app architecture is outside platform control.

The 2.3-minute average is measured at boundary 3 (receiver bank credit) rather than boundary 4 (user-visible reflection), because boundary 4 is bank-app-dependent and not consistent across customers.

What this article does not disclose

To keep this content useful without compromising operational integrity:

- Specific timings for each of the four stages above are not given. The 2.3-minute end-to-end average is the only timing figure Pirate777 publishes.

- The platform’s specific payment processor and acquiring relationships are not named. The architecture is described at the level of the public rail — DuitNow, PayNet, the participating bank pool — rather than the platform’s bilateral integration choices.

- Specific receiving banks are not characterized as “faster” or “slower”. Differences exist but are subject to change, and naming them in a public article risks misleading readers whose own bank’s behaviour may differ.

- Cross-border or non-MYR settlement is not covered. The 2.3-minute average is for MYR slot withdrawals to Malaysian destinations only.

Related guides

- Inside the 2.3-minute average: how Pirate777’s withdrawal architecture actually works — the cluster pillar

- When withdrawals take longer: edge cases, verification steps and bank cut-off times — the exhaustive edge-case list

- My slot withdrawal is stuck: triage steps before contacting Captain’s Support — symptom-first troubleshooting

- Large withdrawals in Malaysia: splits, KYC, rank tiers — for amounts above the standard caps

Frequently Asked Questions

No. DuitNow is operated by Payments Network Malaysia (PayNet) under Bank Negara Malaysia’s regulatory framework. Banks participate on the rail, but the rail itself is shared national infrastructure.

Different settlement model. DuitNow Transfer settles each transaction individually in real time the moment it arrives at the rail. IBG settles transactions in batches at fixed cycles through the business day. Both are bank-to-bank, but the timing characteristics are fundamentally different.

Yes for the rail. PayNet maintains DuitNow service continuously, and participating banks maintain inbound DuitNow availability outside their core banking hours. Some receiving banks reflect inbound credits on their app on a slight delay during off-peak hours, but the credit is on the bank’s books in real time.

Not strictly. Each eWallet operator runs its own near-real-time crediting infrastructure on the inbound side, with direct API integration to Pirate777’s payment layer. The timing characteristics are equivalent to DuitNow Transfer — single-digit minutes — but the rail itself is the eWallet’s own infrastructure, not DuitNow.

You’re seeing the boundary between rail settlement (the credit is on the bank’s books) and user-visible balance update (the bank’s app catching up). Pirate777’s “completed” status fires when the credit has been confirmed at the receiving bank. The user-app reflection is a separate event on the bank’s infrastructure.

The 2.3-minute average covers four stages — submission validation, risk and bonus-completion checks, processor handoff, and rail settlement. The DuitNow rail itself settles in seconds; most of the 2.3 minutes is platform-side outbound verification. Faster outbound verification would tighten the average; the rail is not the bottleneck.

No. Slot withdrawals to bank destinations use DuitNow Transfer (account-to-account). DuitNow QR is for in-person retail and peer-to-peer scanning workflows; it’s not the right tool for platform-to-customer payouts.

18+ only. Play within your limits. If gambling stops being fun, take a break — Pirate777 supports deposit limits, time-outs and self-exclusion. — Pirate777 Team